I get a big kick out of these annual surveys (and we’ve done our fair share of them at TMG). We often use them to validate key messages with clients. I recently came across this one from Deloitte and I was struck by what it was telling us and some of the inconsistencies.

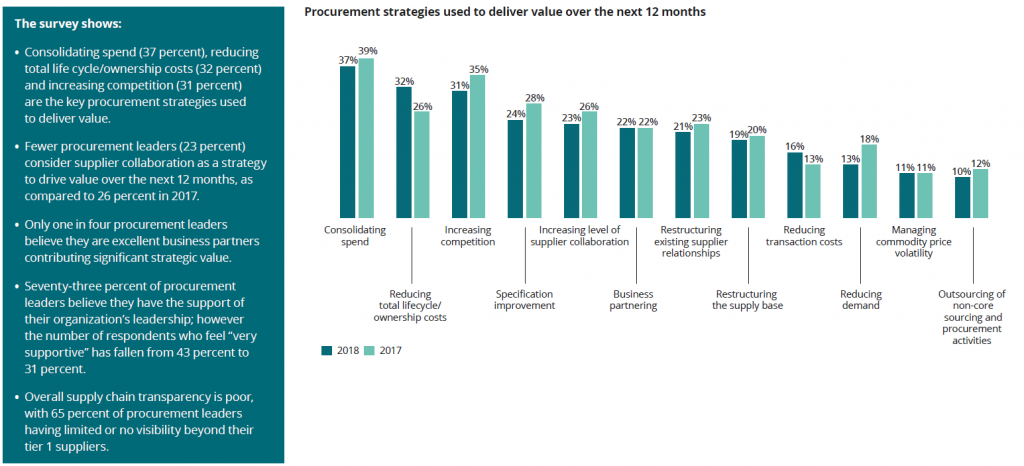

Let’s take a look at the top three strategies used to deliver value. If you are an alumnus of Category Management “U”, an attendee of any of our webinar series, a client or a reader of this blog, you will quickly agree that the basic premise of that question is flawed because it uses the definition of value as defined by Procurement and NOT the stakeholders! This is why we are always and will continue to run into resistance. This is why we will always remain being known as chasing the last nickel from the supplier and not really adding any value. Consolidating spend, increasing competition and my all-time favorite – reducing transaction costs- are not tied to what our stakeholders define as value.

The second observation is that supplier collaboration has decreased as a preferred strategy to deliver value. Nothing could be further from the truth because supplier collaboration is in fact a best Next Practice and has empirically been shown to have significant value for corporations. It is in fact the largest untapped source of value available – if you know how to get at it. This is why we have even changed the term Supplier Relationship Management to Optimization. This particular data point was quite disheartening as it points to a slight regression on this issue and our hope was that in fact this percentage would increase.

Perhaps it’s not that surprising since other potential value generating strategies also suffered a similar fate – Specification Improvement, Business Partnering etc. What is surprising is that given the increasing utilization of RPA, AI, Blockchain etc., more and more procurement leaders are not desperately trying to change the definition of value and a drastic change in their strategies. I don’t want to antagonize anyone but it almost reminds me of the ostrich that buries it’s head in the sand. And the reason I feel comfortable saying that is when I look at the third observation which says that only 25% of procurement leaders believe they are excellent business partners and contribute significant strategic value. Let’s just let that number soak in a little – only 1 in 4! And that number comes from a self-assessment – I wonder what that number would be if the stakeholders were asked that question about the same procurement organizations?

First is the shock that only 25% of us are business partners or adding any strategic value. Second is the shock at the shock because all you have to do is to take a look at what strategies are depicted in the graph above as the ones we are following to deliver value. You will quickly understand that our strategies are still very tactical and trying to deliver tactical goals (last nickel from the supplier). That 25% number is probably generous given the graph above and that’s logical?

This particular graph was a dose of sobering reality that despite so many years of everyone talking about it and much proselytizing from us, we still may have a way to go to fundamentally change the way we think about our function.

{kind=link}